Image

Introduction

In full disclosure, I am currently campaigning for the office of Commissioner of the Revenue in Spotsylvania County, Virginia, with the election scheduled for November 3, 2026. As I continue engaging residents throughout the county, I have observed a growing number of questions concerning real estate assessments, personal property taxation, taxpayer rights, and the responsibilities of local government officials in establishing and managing taxable value. Those questions are legitimate and deserving of thoughtful, factual, and transparent discussion.

Because of the educational nature of Public Agenda, this article is not intended to serve as campaign advocacy. Rather, it is intended to provide a scholarly and practical overview of how localities utilizing real estate and personal property taxation generally conduct assessments, how governing bodies should uphold transparency and fairness in valuation and procurement activities, and how citizens may exercise their rights to foster accountability within local government systems.

Property taxation remains one of the foundational revenue mechanisms utilized by local governments across the United States to fund public education, public safety, infrastructure, emergency services, and other essential governmental functions (Fisher, 2016). Yet despite its importance, many citizens possess only a limited understanding of how assessments are developed, how valuation methodologies operate, and what legal protections exist to ensure fairness and accountability. In democratic governance systems, this awareness gap can weaken public trust and civic participation.

Public administration scholars have long argued that public trust is directly tied to transparency, procedural fairness, and ethical stewardship in government operations (Denhardt & Denhardt, 2015). Consequently, the administration of local taxation must not merely comply with statutory requirements. It must also embody principles of fairness, consistency, openness, and accountability.

The Constitutional and Statutory Foundation of Property Taxation

Property taxation authority in Virginia derives from constitutional and statutory authority. Article X of the Constitution of Virginia establishes the framework for taxation and requires that taxation be uniform upon the same class of subjects within territorial limits (Constitution of Virginia, art. X, § 1). Local governments are then empowered through the Code of Virginia to assess and administer taxes within prescribed legal boundaries.

Commissioners of the Revenue in Virginia are constitutional officers established under Article VII, Section 4 of the Constitution of Virginia. Their responsibilities generally include assessing local taxes, maintaining tax records, administering tax relief programs where authorized, and ensuring compliance with applicable tax laws (Code of Virginia § 15.2-1600).

Importantly, the Commissioner of the Revenue does not establish tax rates. Tax rates are generally established by elected governing bodies such as Boards of Supervisors or City Councils through budgetary and legislative processes. The Commissioner’s role instead centers on equitable administration and assessment integrity.

This distinction matters significantly from a governance perspective because public misunderstanding frequently conflates assessments with tax rate policy decisions. Effective local governance therefore requires clear communication between governing bodies, constitutional officers, and citizens regarding the separate responsibilities each entity holds within the taxation process.

Understanding Real Estate Assessments

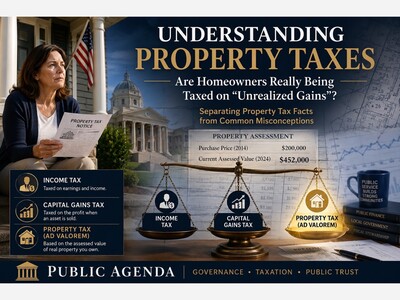

Real estate assessments are intended to estimate the fair market value of property for taxation purposes. Fair market value is generally understood as the price a willing buyer would pay a willing seller in an open and competitive market absent coercion (International Association of Assessing Officers [IAAO], 2013).

Localities commonly utilize three primary methodologies in establishing real estate assessments:

The Sales Comparison Approach

The sales comparison approach evaluates recent sales of similar properties within a comparable geographic and economic market area. Adjustments are often made for square footage, location, condition, improvements, amenities, and lot characteristics.

This method is among the most widely accepted methodologies because it reflects actual market behavior and observable transaction activity (IAAO, 2013).

The Cost Approach

The cost approach estimates the replacement cost of the structure, subtracts depreciation, and adds land value. This methodology is often utilized for specialized properties where comparable sales data may be limited.

The Income Approach

The income approach is generally utilized for income-producing properties such as commercial buildings, apartment complexes, and certain industrial properties. The method estimates value based upon the income-generating potential of the property.

Each methodology possesses strengths and limitations. Consequently, professional assessors frequently utilize multiple approaches simultaneously to improve assessment reliability and equity.

Understanding Personal Property Assessments

Unlike real estate, personal property taxation generally involves movable property such as vehicles, trailers, boats, and certain business equipment.

In Virginia, personal property assessments often rely heavily upon standardized valuation guides, depreciation schedules, and market-based valuation systems authorized by state law or adopted local practices (Code of Virginia § 58.1-3503).

Vehicle assessments commonly utilize pricing services such as the National Automobile Dealers Association guides or comparable market valuation systems. Depreciation schedules may also be employed to account for declining asset value over time.

However, because vehicle markets can fluctuate rapidly due to inflation, supply chain disruptions, or regional demand variations, local governments must continuously evaluate whether assessment methodologies remain equitable and reflective of actual market conditions.

The legitimacy of any assessment system depends upon consistency, procedural fairness, and the availability of meaningful appeal processes.

Transparency and Best Practices in Local Governance

Transparency serves as a cornerstone of democratic legitimacy. Public administration research consistently demonstrates that trust in government increases when citizens perceive governmental processes to be understandable, accessible, and procedurally fair (Yang & Holzer, 2006).

Consequently, governing bodies and constitutional officers should pursue several best practices when administering assessments and utilizing taxpayer funds.

Clear Public Communication

Citizens should have access to understandable explanations regarding:

Complex technical processes should not become barriers to public understanding.

Data Accuracy and Record Accessibility

Citizens should regularly review their property records for errors involving:

Errors in governmental records can produce inaccurate assessments. Local governments therefore possess a stewardship responsibility to maintain accurate and current data systems.

Uniformity and Equity

Uniform application of assessment standards remains legally and ethically essential. Unequal or inconsistent assessments may undermine public confidence and potentially violate constitutional uniformity principles.

The United States Supreme Court has recognized that intentional and systematic disparities in assessments may violate equal protection requirements under certain circumstances (Allegheny Pittsburgh Coal Co. v. County Commission of Webster County, 1989).

Ethical Procurement and Valuation Stewardship

Transparency obligations extend beyond citizen taxation into governmental purchasing decisions involving taxpayer funds.

When local governments purchase real estate, vehicles, technology systems, or other major assets, public leaders should utilize:

Stewardship requires public officials to establish reasonable value prior to expenditure of taxpayer funds.

Public procurement failures have historically generated significant public distrust nationwide due to perceptions of favoritism, waste, or insufficient oversight (Thai, 2009). Consequently, local leaders should prioritize documentation, openness, and procedural rigor throughout acquisition processes.

Taxpayer Rights and Accountability Mechanisms

Citizens possess important rights within democratic taxation systems.

Assessment Appeals

Taxpayers generally possess the right to challenge assessments they believe are inaccurate or inequitable. In Virginia, this may include administrative review processes and appeals to local Boards of Equalization where applicable (Code of Virginia § 58.1-3374).

Taxpayers should maintain documentation supporting their position, including photographs, appraisals, comparable sales, repair estimates, or valuation inconsistencies.

Public Records Access

Citizens may also exercise transparency rights through the Virginia Freedom of Information Act (Code of Virginia § 2.2-3700 et seq.). This legislation generally provides access to many governmental records concerning expenditures, procurement activities, meeting records, and assessment-related processes.

Transparency laws serve as accountability mechanisms designed to preserve public confidence and democratic oversight.

Public Participation

Citizens retain the right to:

Effective governance requires informed and engaged citizenship.

Oversight After Government Purchases

Taxpayer accountability does not end once government expenditures occur. Citizens may continue monitoring:

Stewardship requires continuous oversight, not merely initial approval.

Public Trust, Fairness, and the Role of Ethical Leadership

Modern public administration increasingly emphasizes governance models rooted in public trust, ethical leadership, and citizen-centered administration (Denhardt & Denhardt, 2015).

Assessment systems carry substantial implications for household finances, business sustainability, housing affordability, and citizen perceptions of fairness. Consequently, public officials responsible for administering or overseeing taxation systems must approach their duties with professionalism, neutrality, and integrity.

The principles of fairness, transparency, and stewardship are not merely campaign language or administrative slogans. They represent operational necessities within democratic governance systems.

Fairness requires consistency and impartiality.

Transparency requires openness and understandable processes.

Stewardship requires responsible management of public authority and taxpayer resources.

When citizens believe governmental systems are fair, accountable, and professionally administered, institutional trust strengthens. When transparency weakens or inconsistency emerges, public confidence deteriorates.

Conclusion

Property taxation remains one of the most consequential and visible interactions citizens experience with local government. Because these systems directly affect households, businesses, and community investment, public officials bear a profound responsibility to administer them ethically, transparently, and competently.

Likewise, citizens bear an important civic responsibility to remain informed, engaged, and proactive in exercising their rights within democratic governance structures.

An informed public strengthens accountability.

Transparent systems strengthen legitimacy.

Ethical stewardship strengthens trust.

In an era where confidence in institutions is increasingly tested, local government leaders must continue striving toward governance practices that honor both the law and the public they serve.

References

Allegheny Pittsburgh Coal Co. v. County Commission of Webster County, 488 U.S. 336 (1989).

Code of Virginia § 2.2-3700 et seq. Virginia Freedom of Information Act.

Code of Virginia § 15.2-1600.

Code of Virginia § 58.1-3374.

Code of Virginia § 58.1-3503.

Constitution of Virginia art. VII, § 4.

Constitution of Virginia art. X, § 1.

Denhardt, J. V., & Denhardt, R. B. (2015). The new public service: Serving, not steering (4th ed.). Routledge.

Fisher, R. C. (2016). State and local public finance (4th ed.). Routledge.

International Association of Assessing Officers. (2013). Standard on ratio studies. International Association of Assessing Officers.

Thai, K. V. (2009). International handbook of public procurement. CRC Press.

Yang, K., & Holzer, M. (2006). The performance trust link: Implications for performance measurement. Public Administration Review, 66(1), 114-126. https://doi.org/10.1111/j.1540-6210.2006.00560.x

By Dr. Shellie M. Bowman · Launched a year agoPublic Agenda is a trusted voice at the intersection of democracy, leadership, and public trust, bringing clarity, courage, and conviction to the challenges that shape our common good.SubscribeBy subscribing, you agree Substack's Terms of Use, and acknowledge its Information Collection Notice and Privacy Policy.

Sunny, with a high of 97 and low of 75 degrees. Sunny for the morning, partly cloudy during the afternoon, sunny during the evening, clear overnight.