Image

By Dr Shellie M Bowman Sr

One of the most common questions homeowners ask is both understandable and important:

“If I have not sold my home, why am I pay higher property taxes because the government says my home is worth more?”

The question reflects a genuine concern shared by many homeowners across the United States. As property values have increased in many communities, so too have property tax bills. For many families, especially retirees and those living on fixed incomes, these increases can create real financial pressure.

The concern deserves more than a political slogan or a social media sound bite. It deserves a factual explanation.

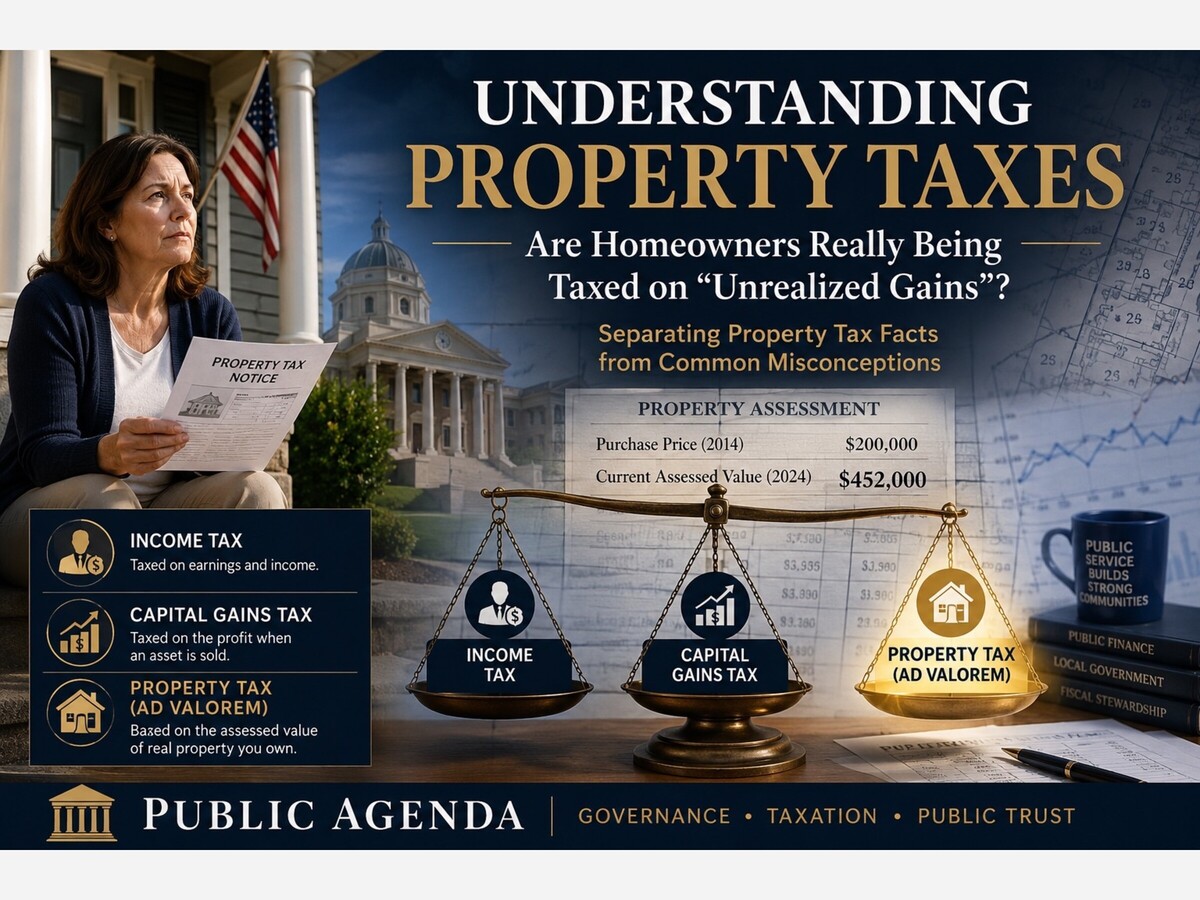

The short answer is no. Homeowners are not paying a capital gains tax on unrealized appreciation. They are paying a local real estate property tax, which is a fundamentally different type of tax.

Understanding that distinction helps explain why many homeowners feel frustrated, even though different tax laws are being applied.

Three Different Types of Taxes

One reason this issue creates confusion is because Americans pay several different types of taxes, each governed by different laws and serving different public purposes.

Income Tax

Income taxes are generally imposed on wages, salaries, self-employment income, business profits, interest, dividends, and other forms of taxable income. If an individual’s income does not increase, the mere appreciation of an asset generally does not increase that person’s income tax liability.

Capital Gains Tax

Capital gains taxes apply differently.

A capital gain generally occurs when a capital asset is sold for more than its adjusted basis. Until that sale occurs, appreciation in value is generally considered an unrealized gain and is not subject to federal capital gains tax. Simply owning an asset that increases in value does not, by itself, create a federal capital gains tax liability (Internal Revenue Service [IRS], 2025).

Real Estate Property Tax

Property taxes operate under an entirely different legal framework.A real estate property tax is:

not a tax on income;

not a tax on income;

not a tax on profit; and

not a capital gains tax.

Instead, it is a local tax imposed on the assessed value of real property.

In Virginia, Article X, Section 2 of the Constitution of Virginia provides that real property is generally assessed at fair market value unless otherwise provided by law. Virginia Code § 58.1-3103 further requires taxable real estate to be assessed at fair market value. Local governing bodies then establish the tax rate applied to those assessments.

Understanding Ad Valorem Taxation

Property taxes are commonly referred to as ad valorem taxes.

Ad valorem is a Latin phrase meaning “according to value.”

Unlike an income tax, which is based on earnings, or a capital gains tax, which is generally based upon the sale of property, an ad valorem tax is based upon the assessed value of the property itself.

As assessed values increase, property taxes may also increase even when the owner has neither sold the property nor received additional income.

Understanding this principle does not necessarily resolve concerns about affordability, but it does explain the legal foundation upon which property taxation operates.

Why Property Taxes Became the Foundation of Local Government

Property taxation developed because real estate has historically provided one of the most stable and predictable tax bases available to local governments.

Unlike wages, business income, or investment assets, land cannot be relocated to another jurisdiction. Consequently, property taxes have long served as the primary means by which local governments finance services that are inherently local, including public education, law enforcement, fire and emergency services, constitutional offices, courts, libraries, parks, and transportation infrastructure.

Whether property taxes remain the most equitable method of financing local government is an appropriate subject for public policy discussion. Understanding why governments rely upon property taxes, however, helps distinguish the purpose of the tax from its financial impact on individual homeowners.

Why Many Homeowners Feel Frustrated

Consider a homeowner who purchased a residence for $200,000 in 2014.

A decade later, the property’s estimated fair market value is $452,000.

Several important facts remain true.

The homeowner has not sold the property.

No capital gain has been realized.

No additional income has been earned.

No proceeds have been received.

Nevertheless, the property’s assessed value may have increased, and the annual property tax bill may increase accordingly.

From the homeowner’s perspective, this can understandably feel similar to paying taxes on money that has never been received.

Legally, however, that is not what is occurring.

The tax is based upon the property’s assessed fair market value, not upon the homeowner’s income or whether the homeowner has realized a gain through the sale of the property.

Recognizing this distinction does not diminish the financial burden many homeowners experience. It simply explains the legal basis upon which local property taxes are assessed.

Assessment and Tax Rates Are Separate Decisions

Another important distinction often receives far less public attention.

The property assessment and the property tax rate are separate components of the local property tax system.

The assessment estimates the property’s fair market value.

The tax rate determines how much tax is levied against that assessed value.

Both influence the final tax bill, but they are separate governmental decisions.

This distinction is particularly important because many states intentionally separate assessment responsibilities from budgetary and tax-rate decisions. Doing so helps preserve objectivity in the valuation process while ensuring elected governing bodies remain publicly accountable for taxation and spending decisions.

Understanding these separate responsibilities enables citizens to participate more effectively in discussions concerning taxation, budgeting, and public finance.

The Real Public Policy Questions

The more meaningful discussion is not whether property taxes are capital gains taxes.

They are not.

Rather, citizens and policymakers should consider questions such as:

Are property assessments accurate and supported by accepted appraisal standards?

Are assessments applied fairly and consistently across similar properties?

Are tax burdens appropriately balanced among residential property owners, commercial property, and other available revenue sources?

Are local tax rates fiscally prudent?

Are property tax relief programs reaching eligible seniors, disabled individuals, disabled veterans, and other qualifying taxpayers?

Should local governments diversify their revenue sources so homeowners are not disproportionately responsible for financing local government?

These questions reach beyond tax administration. They concern the broader principles of public finance, fiscal stewardship, and public trust.

Good Public Policy Begins with Good Information

Healthy democratic institutions depend upon informed citizens.

Property taxation has generated debate throughout American history, and reasonable people will continue to disagree about its scope, administration, and long-term role in financing local government. Those debates should be encouraged. They are most productive, however, when they begin with a shared understanding of the legal framework, the economic principles involved, and the distinction between taxation based on income, realized gains, and assessed property values.

Public confidence in government is strengthened not merely by lower taxes or higher revenues, but by transparent processes, equitable administration, responsible fiscal stewardship, and informed public dialogue.

Good public policy begins with good information.

Reminder of our publishing frequency change

Public Agenda is a weekly publication dedicated to advancing public understanding of governance, taxation, public finance, and civic stewardship through fact-based, scholarly analysis.

References

Constitution of Virginia. art. X, § 2.

International Association of Assessing Officers. (2013). Property assessment valuation (3rd ed.). International Association of Assessing Officers.

Internal Revenue Service. (2025). Topic No. 409: Capital gains and losses. https://www.irs.gov/taxtopics/tc409

Lincoln Institute of Land Policy. (2023). Property tax fundamentals.

https://www.lincolninst.edu

Virginia Code § 58.1-3103. Assessment of real estate at fair market value.

Virginia Department of Taxation. (2025). Real estate tax.

https://www.tax.virginia.gov

A Note to Public Agenda Readers

Beginning with our next publication cycle, Public Agenda will move from two articles per week to one substantive weekly publication.

This change is intentional. Public Agenda has continued to develop as a source of scholarly yet accessible analysis concerning public administration, governance, public finance, and civic life. Moving to a weekly schedule will provide additional time to examine primary documents, verify factual assertions, develop stronger analysis, and ensure that each article is supported by authoritative government, institutional, or peer-reviewed sources.

The goal is not simply to publish less often. It is to publish with greater depth, practical value, and lasting relevance.

Readers can expect one carefully researched article each week that explains how public institutions affect everyday life and helps citizens engage government with greater knowledge and confidence.

Thank you for reading, sharing, and continuing to support Public Agenda.

Public Agenda is free today. But if you enjoyed this post, you can tell Public Agenda that the writing is valuable by pledging a future subscription. You won’t be charged unless payments are enabled.

Follow us on TikTok @DrShelliePublicAgenda

📢 Stay Connected with Public Agenda by Dr. Shellie M. Bowman

Let’s rebuild public leadership together; one insight, one question, one breakthrough at a time.

eLEADt On with Purpose

Smoky haze, with a high of 102 and low of 70 degrees. Smoky haze in the morning, sunny during the afternoon, patchy rain nearby in the evening, smoky haze overnight.

So how do we close the wealth gap? No country has survived a wealth gap as large as the US wealth gap. Why can't politician communicate this to the average person?