Image

Introduction

Public policy often includes ambitious goals designed to encourage participation and inspire long-term thinking. One recent example is the creation of Trump Accounts, a federally authorized investment account that provides eligible children with an initial federal contribution of $1,000. While promoting the program, President Donald J. Trump stated that participating children could become “very wealthy people” as their investments grow over time (The White House, 2026).

That statement raises an important public finance question: Can a one-time $1,000 investment reasonably be expected to create wealth?

This article does not evaluate the political merits of the legislation or the intentions behind the program. Instead, it applies established principles of finance, including the time value of money, compound interest, and inflation adjustment, to examine what the initial federal contribution could reasonably become under transparent assumptions. Public confidence in fiscal policy is strengthened when claims are evaluated using verifiable data, clearly stated assumptions, and reproducible calculations.

This analysis is provided for educational purposes only and should not be interpreted as investment, tax, or financial advice.

Understanding Trump Accounts

The One Big Beautiful Bill Act established Trump Accounts as tax-advantaged investment accounts for eligible children. Under current federal guidance, qualifying children receive a one-time federal contribution of $1,000, while parents, relatives, employers, and others may make additional contributions within statutory limits (Internal Revenue Service [IRS], 2026; U.S. Department of the Treasury, 2026).

The policy reflects a well-established financial principle: investments made earlier have more time to benefit from compound growth than investments made later. The initial contribution is intended to provide children with an early financial asset that may grow over time through investment returns.

Whether that initial investment alone can reasonably be described as creating wealth is a question that can be examined mathematically.

Methodology

To evaluate the financial implications of the initial federal contribution, this analysis models a single hypothetical scenario using transparent assumptions.

The model assumes:

Initial federal contribution: $1,000

Investment horizon: 18 years

Nominal annual investment return: 8.0 percent

Average annual inflation: 2.3 percent

Annual compounding

No additional contributions

No withdrawals

No taxes, fees, or investment expenses

The future value of the investment is calculated using the standard compound interest equation:

[

FV = PV(1+r)^n

]

where FV represents future value, PV represents present value, r represents the annual rate of return, and n represents the number of years invested.

These assumptions are intended to illustrate the mechanics of compound growth rather than predict future investment performance.

The Mathematics of Compounding

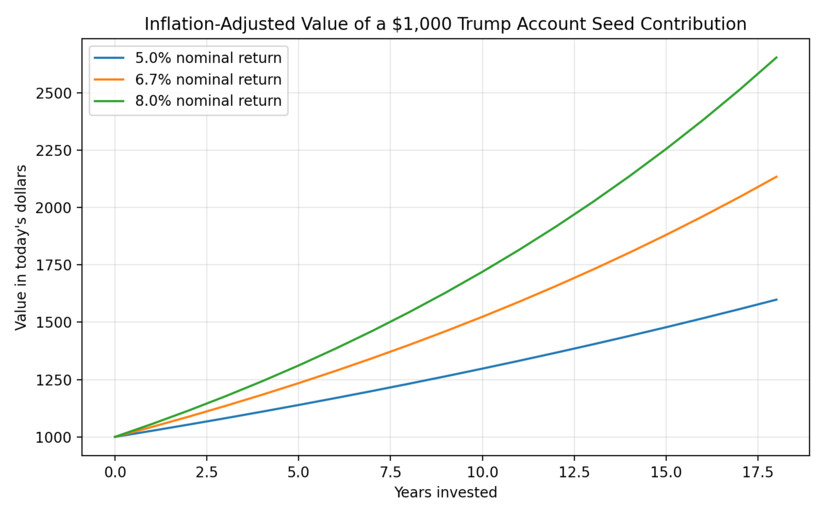

Applying the assumptions above, a one-time investment of $1,000 earning an average annual return of 8 percent for 18 years produces a nominal ending value of approximately $3,996.

Although nearly quadrupling an investment appears impressive, financial analysis requires distinguishing between nominal dollars and real purchasing power.

Assuming long-term inflation averages 2.3 percent annually, the purchasing power of that projected balance is approximately $2,654 in today’s dollars.

Figure 1 illustrates this relationship by comparing nominal investment growth with inflation-adjusted purchasing power over the eighteen-year investment period.

The distinction between nominal and real values is fundamental in economics. Nominal values describe the number of dollars accumulated, whereas real values measure what those dollars can actually purchase after accounting for inflation. For households planning for long-term financial security, purchasing power generally provides the more meaningful measure of economic progress.

Can Compound Interest Alone Create Wealth?

Compound interest has been described for generations as one of the most powerful principles in finance because investment earnings generate additional earnings over time. However, compound growth depends upon four primary variables

Initial principal

Additional contributions

Rate of return

Time

The Trump Account provides the first variable through the federal seed contribution. The remaining variables depend upon future investment performance, the account owner’s behavior, and the passage of time.

The mathematics demonstrate that a relatively small principal, even when invested successfully, grows modestly during an eighteen-year period if no additional contributions are made. This observation should not be interpreted as a criticism of the program. Rather, it reflects the mathematical reality that compound interest becomes increasingly powerful over multiple decades, particularly when accompanied by regular contributions.

Consequently, the appropriate public policy question is not whether compound interest works. It unquestionably does. The more relevant question is whether the initial $1,000 contribution, standing alone, is sufficient to produce what most Americans would reasonably describe as wealth.

Defining Wealth

The answer depends largely upon how the word wealth is defined.

Economists generally define wealth as net worth, representing the value of assets after liabilities have been considered. The Federal Reserve’s Survey of Consumer Finances consistently demonstrates that household wealth reflects the accumulation of multiple assets over long periods of time rather than the balance of a single investment account (Board of Governors of the Federal Reserve System, 2023).

Using that framework, a projected balance of approximately $3,996, or roughly $2,654 after adjusting for inflation, would generally be viewed as an early financial asset rather than wealth itself.

That distinction is significant. Assets contribute to wealth, but a single asset does not necessarily constitute wealth.

A Balanced Perspective

Viewed objectively, the initial federal contribution provides eligible children with something many Americans never receive: an opportunity to begin investing at birth. That opportunity has value. It introduces the principles of ownership, long-term investing, and compound growth early in life.

At the same time, the mathematical analysis suggests that the initial $1,000 contribution alone is unlikely to produce wealth by age eighteen under the assumptions presented in this article. Meaningful wealth accumulation would generally require one or more of the following:

Additional contributions over many years.

Higher-than-assumed long-term investment returns.

A substantially longer investment horizon.

A combination of all three.

Accordingly, the Trump Account may be better understood as a financial foundation rather than a complete wealth-building strategy.

Conclusion

Financial transparency requires that public policy claims be evaluated using evidence rather than assumption. The mathematics of compound interest clearly demonstrate that investing early provides measurable advantages, and the creation of Trump Accounts may encourage long-term financial participation among eligible children.

However, the analysis also demonstrates that the initial federal contribution should not be viewed in isolation. A one-time $1,000 investment, even under favorable assumptions, grows to approximately $3,996 over eighteen years, with an inflation-adjusted purchasing power of roughly $2,654.

These findings neither endorse nor criticize the policy. Rather, they provide context for understanding what the initial investment may reasonably accomplish. In public finance, transparency is strengthened when citizens understand both the promise and the practical limitations of financial programs. Sound policy discussions are best served when public claims are examined through objective analysis, clearly stated assumptions, and verifiable evidence.

Figure 1. Projected nominal and inflation-adjusted growth of a one-time $1,000 federal contribution over an 18-year investment horizon under the assumptions used in this analysis. The figure is illustrative and does not predict future investment performance.

References

Board of Governors of the Federal Reserve System. (2023). Changes in U.S. family finances from 2019 to 2022: Evidence from the Survey of Consumer Finances.

Internal Revenue Service. (2026). Treasury, IRS issue guidance on Trump Accounts established under the Working Families Tax Cuts Act.

The White House. (2026). President Trump rings in Trump Accounts with historic opening bell ceremony from the Oval Office.

U.S. Department of the Treasury. (2026). Treasury launches Trump Accounts to expand investment opportunities for American families.

Overcast, with a high of 86 and low of 73 degrees. Don't forget your umbrella! Overcast in the morning, patchy rain nearby in the afternoon, light rain shower for the evening, overcast overnight.