Image

SUMMARY

Government budgets are among the most important public documents produced each year because they reveal how public institutions intend to allocate resources, deliver services, and fulfill their responsibilities to the communities they serve. Citizens do not need to be accountants to understand government budgets; they need a framework for asking informed questions and interpreting publicly available information.

INTRODUCTION

Imagine attending a public meeting where elected officials are debating a budget increase of several million dollars. One speaker argues that government spending is out of control. Another insists the increase is necessary to maintain essential services. A third points to a large capital project and questions whether taxpayers can afford it. By the end of the discussion, most citizens leave with strong opinions but little understanding of what the budget actually says.

This scenario plays out in communities across the United States every year. Government budgets frequently become the focus of public debate, yet few citizens ever read the documents themselves. Those who attempt to do so are often met with hundreds of pages of tables, charts, forecasts, appropriations, and financial terminology that can appear intimidating to anyone without a background in accounting or finance.

This is understandable. Government budgets are complex documents. However, they are also among the most important public documents produced each year because they reveal how public institutions intend to allocate resources, deliver services, and fulfill their responsibilities to the communities they serve. The Government Finance Officers Association (2024) describes budgeting as one of the most important tools for translating community priorities into public action. In many respects, a budget is more than a financial document. It is a statement of priorities, values, obligations, and tradeoffs.

The good news is that citizens do not need to be accountants to understand government budgets. They simply need a framework for asking the right questions and interpreting the information presented.

WHAT IS A GOVERNMENT BUDGET?

A government budget is a formal plan that estimates revenues and authorizes expenditures for a specific fiscal period. Public budgeting scholars have long argued that budgets serve multiple purposes simultaneously. They function as financial plans, policy instruments, management tools, and mechanisms of public accountability (Rubin, 2023).

Unlike private-sector budgets, government budgets are not designed primarily to maximize profit. Instead, they allocate resources to achieve public purposes such as education, public safety, infrastructure maintenance, environmental protection, and social services. As Wildavsky and Caiden (2004) observed, budgeting is fundamentally a process of deciding who receives public resources, for what purposes, and under what conditions.

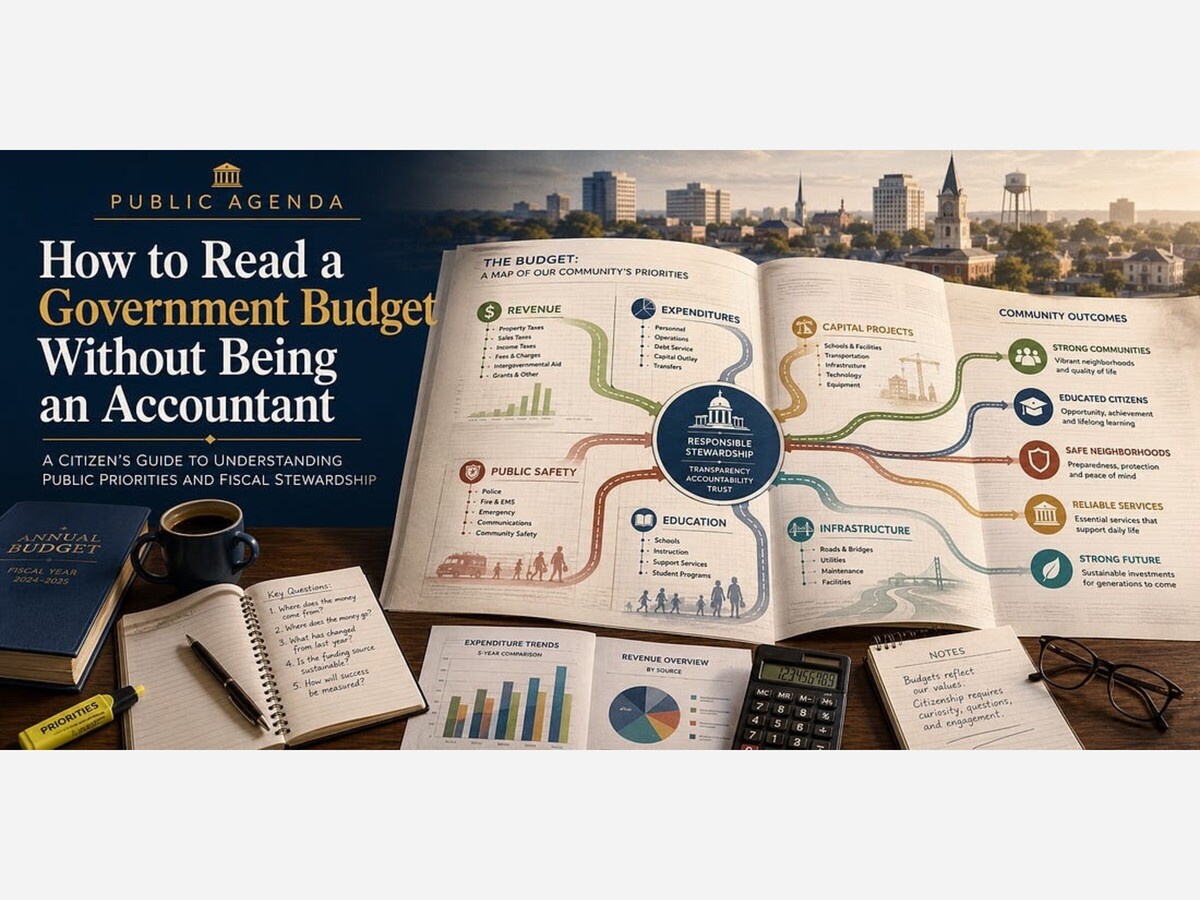

Understanding a government budget begins with recognizing that every budget answers two basic questions: 1. Where does the money come from? 2. Where does the money go?

Everything else is detail.

STEP ONE: START WITH REVENUE

Most citizens begin reading a budget by looking at expenditures. A better approach is to begin with revenue because revenue determines what government can realistically afford.

Government revenues generally come from several sources: - Taxes (property, sales, income, business, excise) - Fees and charges - Intergovernmental revenue - Grants

When reviewing revenue, citizens should ask: Is this revenue recurring or one-time?

Recurring revenues generally provide greater fiscal stability. One-time revenues may temporarily increase funding but often cannot support long-term obligations (GFOA, 2024). Sustainable government operations depend on matching recurring expenditures with recurring revenue sources (GAO, 2023).

STEP TWO: FOLLOW THE EXPENDITURES

After understanding revenue, attention should shift to expenditures. Expenditures reveal governmental priorities.

Common expenditure categories include: - Personnel - Public safety - Education - Public works - Debt service - Capital projects

Budgets reveal priorities more clearly than speeches.

STEP THREE: UNDERSTAND THE DIFFERENCE BETWEEN OPERATING AND CAPITAL BUDGETS

Operating budget: funds day-to-day activities necessary to deliver services (employee salaries, utilities, fuel, office supplies, routine maintenance).

Capital budget: funds major long-term investments (school construction, road expansions, public facilities, water and sewer infrastructure, technology modernization projects).

The distinction matters because capital projects are often financed differently and may involve debt financing or dedicated funding sources (ICMA, 2023).

STEP FOUR: LOOK FOR TRENDS RATHER THAN SINGLE NUMBERS

Meaningful analysis requires examining trends over time.

Compare: - Current year versus prior year - Five-year expenditure trends - Revenue growth patterns - Population changes - Inflation rates - Service demand increases

Single-year increases or decreases can be misleading without context (Congressional Budget Office, 2024).

STEP FIVE: ASK FIVE CRITICAL QUESTIONS

Effective budgeting requires measurable outcomes, performance measures, strategic goals, and accountability mechanisms (Moynihan, 2008; GFOA, 2024).

STEP SIX: DISTINGUISH FACTS FROM OPINIONS

Budgets contain facts. Political arguments about budgets contain interpretations.

Informed citizens examine original documents before accepting conclusions. This requires curiosity, critical thinking, and willingness to review publicly available information. Public accountability depends on access to information and the ability to interpret it (Grimmelikhuijsen & Meijer, 2014).

CONCLUSION

Government budgets reveal how institutions intend to fulfill responsibilities to their communities. Citizens do not need accounting degrees to understand them; they need informed questions and engagement with the information presented. Understanding revenue, expenditures, trends, and outcomes strengthens democratic participation and accountability. Budgets are public declarations of priorities, responsibilities, and commitments.

REFERENCES

Congressional Budget Office. (2024). The budget and economic outlook: 2024 to 2034. U.S. Government Printing Office.

Government Accountability Office. (2023). The federal government’s long-term fiscal outlook: Fiscal stewardship and sustainability. U.S. Government Accountability Office.

Government Finance Officers Association. (2024). Best practices in public budgeting. Government Finance Officers Association.

Grimmelikhuijsen, S., & Meijer, A. J. (2014). Effects of transparency on the perceived trustworthiness of a government organization: Evidence from an online experiment. Journal of Public Administration Research and Theory, 24(1), 137–157.

International City/County Management Association. (2023). Local government budgeting principles and practices. ICMA.

Moynihan, D. P. (2008). The dynamics of performance management: Constructing information and reform. Georgetown University Press.

Rubin, I. S. (2023). The politics of public budgeting: Getting and spending, borrowing and balancing (10th ed.). CQ Press.

Wildavsky, A., & Caiden, N. (2004). The new politics of the budgetary process (5th ed.). Pearson.

Public Agenda is free today. But if you enjoyed this post, you can tell Public Agenda that the writing is valuable by pledging a future subscription. You won’t be charged unless payments are enabled.

Follow us on TikTok @DrShelliePublicAgenda

📢 Stay Connected with Public Agenda by Dr. Shellie M. Bowman

Let’s rebuild public leadership together; one insight, one question, one breakthrough at a time.

eLEADt On with Purpose.

Sunny, with a high of 98 and low of 73 degrees. Sunny in the morning, partly cloudy in the afternoon and evening, clear overnight.