Image

By Dr Shellie M Bowman Sr

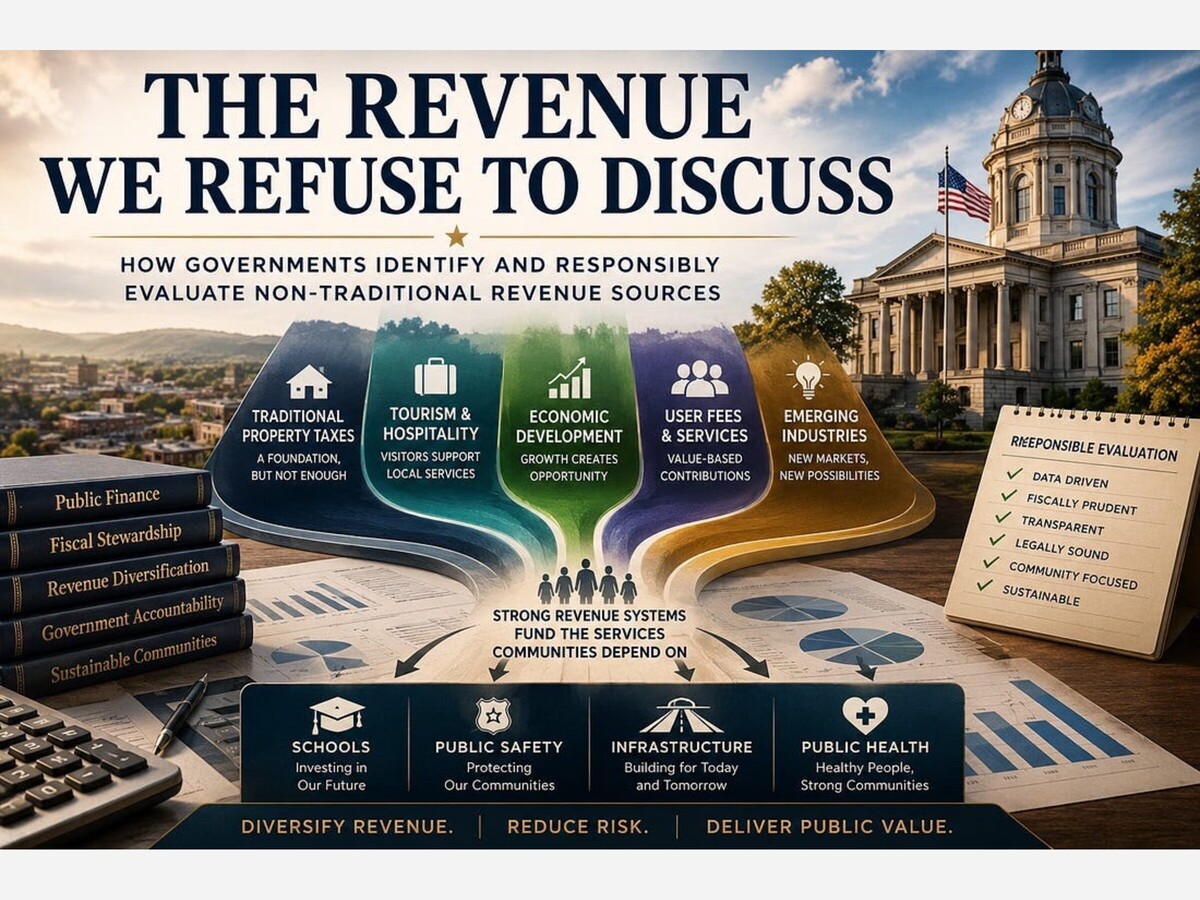

Public conversations about government finance often begin and end with taxes. Citizens debate property tax rates, sales taxes, fees, and government spending. Yet public administrators face a more fundamental challenge: how to build revenue systems capable of sustaining essential public services in a changing economy.

Schools, public safety, transportation infrastructure, public health programs, and economic development initiatives all depend upon stable and reliable revenue streams. As service demands increase and traditional revenue sources become strained, governments are increasingly confronted with a difficult question: should they continue relying upon familiar revenue mechanisms, or should they explore emerging revenue opportunities that may offer additional fiscal capacity?

This question is not new. Public finance scholars have long argued that governments benefit from revenue systems that are diversified rather than overly dependent upon a single source of funding. Revenue diversification has been associated with improved fiscal stability, increased resilience during economic downturns, and a greater ability to sustain public services during periods of financial stress (Yan, 2019; Janson & Marlowe, 2023).

One of the most visible examples of fiscal innovation in recent years has been the emergence of cannabis taxation. While debates surrounding cannabis legalization often focus on criminal justice, public health, or personal liberty, the public administration implications are equally significant. Cannabis taxation provides a useful case study for understanding how governments evaluate non-traditional revenue sources and the opportunities and risks associated with revenue diversification.

The broader lesson extends far beyond cannabis. It is ultimately a lesson about fiscal stewardship, revenue resilience, and the responsibilities of modern government.

Local governments across the United States face increasing fiscal pressures. Rising infrastructure costs, public safety demands, employee compensation needs, inflationary pressures, and expanding service expectations continue to place strain on local budgets.

Historically, many jurisdictions have relied heavily on property taxes and other traditional revenue sources to fund government operations. While these revenue streams remain important, dependence upon a narrow set of funding mechanisms can create vulnerability during periods of economic disruption.

Recent public finance research suggests that revenue diversification can strengthen fiscal health and improve a government’s ability to withstand economic shocks. Yan (2019) found that diversified revenue structures contribute positively to fiscal health during economic downturns. Similarly, Janson and Marlowe (2023) observed that diversified local revenue portfolios are generally associated with greater revenue stability over time.

The principle is straightforward. Just as investors often diversify financial portfolios to reduce risk, governments can diversify revenue portfolios to improve fiscal resilience.

This does not mean pursuing every available revenue source. Instead, it requires governments to evaluate emerging opportunities responsibly, transparently, and in a manner consistent with community values and public priorities.

Cannabis taxation offers one of the clearest examples of revenue diversification in modern public finance.

Since legalizing adult-use cannabis, Colorado has generated billions of dollars in cannabis-related tax and fee revenue. According to the Colorado Department of Revenue, cannabis sales generated more than $236 million in tax and fee revenue during calendar year 2025, bringing cumulative collections since legalization to more than $3.1 billion (Colorado Department of Revenue, 2026). Colorado’s Legislative Council Staff reported that the state collected approximately $231.1 million from marijuana taxes during fiscal year 2024-2025 (Colorado Legislative Council Staff, 2026).

Importantly, cannabis revenue was not simply absorbed into a general fund without purpose. Colorado directed portions of cannabis-related revenues toward education, school construction, regulatory functions, and local government support. Historically, a portion of retail marijuana tax revenues was allocated directly to local governments based upon sales activity occurring within their jurisdictions (Colorado Legislative Council Staff, 2026; Colorado General Assembly, n.d.).

Illinois adopted a different approach. Under Illinois law, local governments may impose local cannabis-related taxes in addition to state cannabis taxes. Municipalities and counties that permit adult-use cannabis businesses may receive direct fiscal benefits from local taxation and revenue-sharing mechanisms (Illinois Department of Revenue, 2026).

These examples demonstrate an important public administration principle: governments can create new revenue streams without increasing dependence upon existing tax structures.

Whether one supports or opposes cannabis legalization is ultimately a separate policy question. The public finance lesson remains the same. Governments continually evaluate emerging industries and economic activities as potential contributors to public revenue.

Discussions of cannabis taxation often fail to distinguish between medical and recreational markets.

This distinction matters because the fiscal objectives of these programs differ significantly.

Medical cannabis programs are generally designed around patient access, healthcare considerations, and therapeutic use. Tax structures within medical cannabis systems are often intentionally limited to avoid increasing costs for patients who rely upon cannabis for medical treatment.

Adult-use or recreational cannabis systems typically serve a different fiscal function. These programs often incorporate excise taxes, retail taxes, and local-option taxes specifically designed to generate public revenue.

Illinois provides a useful example. Local cannabis-specific taxes apply to adult-use cannabis sales, while medical cannabis transactions are generally excluded from many local cannabis taxation provisions (Illinois Department of Revenue, 2026).

For public administrators, this distinction underscores the importance of understanding the policy objectives associated with different revenue mechanisms. Revenue generation may be a primary objective in one system while remaining a secondary consideration in another.

The Colorado experience also highlights an important caution.

Emerging revenue sources should not be viewed as permanent solutions to fiscal challenges.

While Colorado generated substantial cannabis revenues following legalization, recent reports indicate that cannabis-related revenues have become less predictable as markets matured, prices declined, and consumer behavior evolved. State policymakers have increasingly confronted questions regarding the sustainability of cannabis-related revenue streams and the extent to which government programs should rely upon them (Colorado Public Radio, 2025; Axios Denver, 2026).

Michigan’s experience offers similar lessons. In 2026, local governments received nearly $94 million in marijuana excise tax distributions. However, several communities experienced reductions in distributions compared to prior years due to market changes and declining license activity (Big Rapids News, 2026).

These developments reinforce a broader principle of fiscal management: revenue diversification should enhance resilience rather than create new forms of dependency.

A revenue source that appears robust today may become volatile tomorrow.

Effective public administrators recognize this reality and avoid structuring government finances around assumptions of perpetual growth.

Cannabis taxation is only one example of fiscal innovation.

Across the United States, governments routinely explore alternative revenue strategies, including tourism taxes, lodging taxes, meals taxes, special assessment districts, economic development initiatives, user fees, public-private partnerships, and industry-specific taxes.

The objective is not simply to collect more revenue.

The objective is to create revenue systems capable of supporting public value while maintaining fiscal stability.

Recent research on fiscal resilience suggests that revenue diversification contributes positively to government recovery and renewal following economic disruptions (Kim, 2023; Yan, 2019). International Monetary Fund research similarly indicates that tax revenue diversification can reduce revenue volatility and strengthen fiscal resilience (Dabla-Norris et al., 2020).

In practical terms, this means governments should continuously evaluate whether their revenue structures reflect the realities of modern economies.

Communities that depend excessively upon a narrow range of revenue sources may find themselves vulnerable when economic conditions change. Communities with diversified revenue portfolios are often better positioned to adapt.

The debate over cannabis taxation often focuses on the wrong question.

The most important question is not whether cannabis should or should not be legalized.

The more important question is what governments can learn from jurisdictions that have successfully evaluated emerging revenue opportunities.

Cannabis taxation demonstrates both the promise and limitations of fiscal innovation. It illustrates how governments can diversify revenue streams, support public priorities, and reduce pressure on traditional funding sources. At the same time, it reminds public administrators that no revenue source is immune from market volatility or economic change.

The broader lesson is clear.

Fiscal resilience is not achieved by relying more heavily on existing taxpayers. Fiscal resilience is achieved by understanding revenue systems, evaluating new opportunities responsibly, and constructing diversified revenue portfolios capable of sustaining public value over time.

The most successful governments do not simply manage taxes.

They understand revenue systems.

When most people think about government revenue, they think about taxes. Yet the real challenge facing public administrators is much broader. Every community must determine how to sustainably fund schools, public safety, infrastructure, public health, and other essential services while remaining accountable to taxpayers.

The lesson from cannabis taxation is not that every community should embrace cannabis legalization. Communities will continue to make different decisions based on their values, priorities, and public policy objectives.

The lesson is that effective governments remain willing to evaluate new ideas, study emerging economic opportunities, and responsibly assess whether alternative revenue sources can strengthen fiscal resilience.

Fiscal stewardship requires more than balancing budgets. It requires understanding how revenue systems function, where vulnerabilities exist, and how communities can reduce dependence upon any single source of funding.

In the end, the strongest governments are not those that simply collect revenue. They are those that thoughtfully align revenue systems with the public value they seek to create.

Colorado Department of Revenue. (2026). Marijuana tax reports. https://cdor.colorado.gov/data-and-reports/marijuana-data/marijuana-tax-reports

Colorado Department of Revenue. (2026). Marijuana sales generate over $236M in tax, fee revenue figures for 2025. https://tax.colorado.gov/press-release/marijuana-sales-generate-over-236m-in-tax-fee-revenue-figures-for-2025

Colorado Legislative Council Staff. (2026). Marijuana revenue in the state budget. Colorado General Assembly. https://content.leg.colorado.gov/publications/marijuana-revenue-state-budget

Dabla-Norris, E., Lima, F., & Sollaci, A. (2020). Fiscal resilience building: Insights from a new tax diversification measure. International Monetary Fund.

Illinois Department of Revenue. (2026). Cannabis tax frequently asked questions. https://tax.illinois.gov/research/taxinformation/other/cannabis-tax-frequently-asked-questions.html

Illinois Department of Revenue. (2026). Cannabis taxes. https://tax.illinois.gov/research/taxinformation/other/cannabis-taxes.html

Janson, W., & Marlowe, J. (2023). Diversification and stability in Illinois local government revenues. Illinois Municipal Policy Journal, 8(1), 61-80.

Kim, Y. (2023). Fiscal resilience as a strategic response to economic shocks. American Review of Public Administration. Advance online publication.

Yan, W. (2019). Impacts of revenue diversification and revenue elasticity on local fiscal health. State and Local Government Review, 51(2), 91-102.

Public Agenda is free today. But if you enjoyed this post, you can tell Public Agenda that the writing is valuable by pledging a future subscription. You won’t be charged unless payments are enabled.

Follow us on TikTok @DrShelliePublicAgenda

📢 Stay Connected with Public Agenda by Dr. Shellie M. Bowman

Let’s rebuild public leadership together; one insight, one question, one breakthrough at a time.

eLEADt On with Purpose.

Sunny, with a high of 91 and low of 68 degrees. Sunny in the morning, clear overnight.