Image

Communities across the United States periodically revisit the question of whether adultentertainment establishments should be permitted within their boundaries. The debate is often framed in moral, cultural, or public safety terms. Far less frequently discussed is the narrow public finance question: do strip clubs meaningfully improve local government revenue?

The answer is more complicated than either supporters or opponents often suggest. Strip clubs can generate measurable local tax revenue through property taxes, sales taxes, meals taxes, admissions taxes, business license fees, and alcohol taxes. However, the amount of revenue generated is usually modest relative to the size of an entire local government budget. Whether a locality permits or prohibits such establishments generally depends less on fiscal need and more on state law, local zoning authority, and community values.

In practice, local governments that permit strip clubs often realize some additional revenue, particularly in hospitality-oriented urban areas. Yet there is little evidence that such establishments transform a locality’s finances or meaningfully reduce the tax burden on homeowners.

A useful comparison can be made between San Diego County, California, which allows adultentertainment establishments in limited areas, and Prince William County, Virginia, which effectively prohibits them through zoning and land use restrictions.

According to a regional economic study commissioned in San Diego County, the county’s eleven strip clubs collectively generated approximately $35.2 million in direct annual revenue and roughly $70.4 million in broader economic impact when secondary spending was included (San Diego Hospitality and Entertainment Coalition, 2016). The establishments produced local revenue through sales taxes, business license taxes, property taxes, alcohol-related taxes, and employment. Averaged across the eleven clubs, each establishment generated approximately $3.2 million in annual gross revenue.

Even under this comparatively favorable scenario, the fiscal impact remained relatively small in relation to San Diego County’s overall budget and tax base. San Diego County’s annual operating budget exceeds $8 billion (County of San Diego, 2025). Thus, even if every dollar of direct club revenue were taxed at a local rate of several percentage points, the resulting public revenue would amount to only a tiny fraction of one percent of county revenue.

By contrast, Prince William County has no strip clubs because local zoning ordinances do not provide a viable location for adult entertainment establishments. The county instead relies on more traditional commercial activity, such as retail, data centers, restaurants, hospitality, and mixed-use development. Prince William County’s adopted fiscal year 2025 budget exceeds $2 billion without any reliance on adultentertainment tax revenue (Prince William County, 2025).

This comparison suggests that local governments do not need strip clubs in order to maintain a healthy revenue base. A county or city with strong commercial growth, diversified land use, and a broad property tax base can produce substantially more revenue through conventional economic activity.

The more relevant question for public administrators is not whether strip clubs generate any revenue. They do. The more important question is whether the amount of revenue generated is sufficient to outweigh the locality’s other policy concerns.

Scholarly literature suggests that adultentertainment venues may generate localized economic activity, particularly in convention, tourism, and entertainment districts. West (2006) found that many citizens recognize the potential of such establishments to create jobs and tax revenue, especially in urban areas seeking redevelopment. Similarly, Henry (2003) found that governments receive revenue through business licensing, sales taxes, and associated commercial activity in Las Vegas.

However, the same literature also notes that the fiscal benefit is often overstated. Strip clubs are generally small, niche businesses. Even if a locality imposed a special admissions tax or entertainment tax, the total revenue would rarely rival what could be produced by a large retail center, office park, mixed-use development, industrial facility, or data center campus.

For example, a single large data center or regional shopping corridor can produce millions of dollars annually in machinery and tools taxes, business property taxes, meals taxes, and employment-related revenue. By comparison, a strip club may generate several hundred thousand dollars annually in local tax revenue, depending on the locality’s tax structure and the number of patrons.

The legal question of whether strip clubs may be allowed is equally important. In the United States, local governments generally cannot authorize strip clubs unless state law permits adult entertainment businesses. States establish the broad legal framework, while counties and cities determine whether, where, and how such establishments may operate.

Some states expressly permit adultentertainment businesses, subject to local zoning and licensing. In those states, counties, and cities may adopt ordinances regulating location, hours, signage, alcohol sales, distance from schools or churches, and other operational details. Local governments often use zoning authority to confine such establishments to industrial or highway-commercial districts.

Other states permit local governments to prohibit strip clubs entirely through zoning. Courts have generally upheld these restrictions if the locality leaves open some theoretical avenue for adult entertainment somewhere within the jurisdiction. Consequently, many suburban counties effectively prohibit strip clubs by adopting land use rules that make them impractical or impossible.

Virginia is an example of a state where localities possess significant zoning authority over adultbusinesses. Virginia law does not require counties or cities to allow strip clubs. Instead, counties and cities may regulate or prohibit them through local ordinances pursuant to Virginia Code § 15.2-2280 et seq. and Virginia Code § 15.2-920.1. As a result, some Virginia localities contain adult entertainment venues, while many others do not.

This distinction matters because the decision is usually made at the county or city level, not by the state legislature alone. A county board of supervisors or city council can effectively determine whether such establishments are allowed through zoning maps, special use permits, and business licensing rules.

For public administrators, the issue ultimately becomes one of stewardship and transparency. Citizens deserve an honest discussion about the true fiscal value of any proposed business activity. If a locality is considering whether to permit strip clubs, residents should understand that the establishments may provide some additional revenue, but not enough to fundamentally reshape the local tax structure.

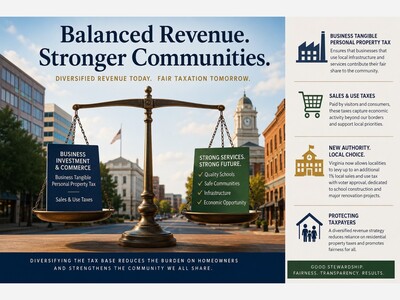

A locality seeking to reduce pressure on homeowners is generally more likely to succeed by diversifying revenue streams through broader commercial development, tourism, technology investment, mixed-use growth, and other sectors capable of producing a larger and more stable tax base.

Strip clubs may generate revenue, but they are not a substitute for comprehensive economic development policy.

If a locality truly wants to generate enough revenue to provide noticeable tax relief to homeowners, the most effective approach is not to rely on small niche industries or continued increases in residential property taxes. Instead, local governments are generally more successful when they pursue a broader and more balanced revenue structure.

Public finance research consistently shows that communities are strongest when they do not depend too heavily on any one source of revenue. A locality that leans too heavily on homeowners often places increasing pressure on residents without creating a corresponding increase in visible public value. By contrast, localities that broaden their commercial activity, encourage economic growth, and create new nonresidential sources of revenue are often better positioned to stabilize or reduce the burden on homeowners (International City/County Management Association, 2021; Levy, 2019).

The central lesson is that there are options beyond repeatedly turning to residential property taxes. Local governments may choose to pursue a more diversified mix of commercial, tourism, business, and other nonresidential revenue sources depending on the character of the community and the authority provided by state law.

In Virginia, some of the most fiscally successful localities have demonstrated that a broader revenue structure can make a meaningful difference. These localities have often reduced pressure on homeowners not by raising taxes faster, but by creating a stronger balance between residential taxpayers and other sources of local revenue (Mangum Economics, 2024; Loudoun County, 2025).

For public administrators, the question is not simply how to collect more money. The more important question is whether the tax structure is fair, transparent, sustainable, and balanced. Citizens deserve to know that local governments have choices, and that homeowners do not have to bear an ever-growing share of the burden.

A locality seeking long-term tax relief should therefore begin by asking whether its current revenue structure is overly dependent on residents and whether there are responsible opportunities to create a more balanced approach.

Henry, C. (2003). The economic impact of the adult dance establishments on local governments and the Las Vegas economy (Master’s thesis, University of Nevada, Las Vegas).

San Diego Hospitality and Entertainment Coalition. (2016). Economic impact study of adult entertainment establishments in San Diego County.

West, D. M. (2006). Public assessments of the adult entertainment industry. Economic Development Quarterly, 20(1), 5-17.

Virginia Code § 15.2-2280 et seq. (Zoning ordinances).

Virginia Code § 15.2-920.1. (Regulation of adultbusinesses).

County of San Diego. (2025). Adopted operational plan for fiscal year 2025–26.

International City/County Management Association. (2021). Local economic resilience and diversified revenue strategies.

Levy, J. M. (2019). Contemporary urban planning (11th ed.). Routledge.

Loudoun County. (2025). Fiscal year 2025 adopted budget.

Mangum Economics. (2024). The economic and fiscal impact of data centers in Virginia.

Prince William County. (2025). Fiscal year 2025 adopted budget.

Public Agenda is free today. But if you enjoyed this post, you can tell Public Agenda that the writing is valuable by pledging a future subscription. You won’t be charged unless payments are enabled.

Follow us on TikTok @DrShelliePublicAgenda

📢 Stay Connected with Public Agenda by Dr. Shellie M. Bowman

Let’s rebuild public leadership together; one insight, one question, one breakthrough at a time.

eLEADt On with Purpose.

Please write your comments below. If you want more articles like this please like them. Hashtag and Share our articles with others.

Sunny, with a high of 89 and low of 69 degrees. Sunny for the morning, clear in the afternoon and evening,